Our director of Grupo Tributario, Andrea Bobadilla, talked to Diario Financiero about the implications that the tax reform promoted by Donald Trump in the United States could bring and how it could affect our country.

The “Big Beautiful Bill” establishes rate increases for taxpayers coming from countries that apply discriminatory taxes to U.S. citizens, which has raised concerns about the possibility of Chile joining this group.

The almost five months of the administration of the President of the United States, Donald Trump, have been a real roller coaster for the world.

There are plenty of reasons, such as the disruptions that he has generated in the migratory flow to the United States or the heated trade war with different countries, mainly China.

But there is a focus of uncertainty that is in the sights of Chilean companies, individuals and tax advisors, which promises to change the rules of the game and, eventually, increase their tax burden.

It is Trump’s tax reform, called the Big Beautiful Bill (“Big Beautiful Bill”), which mainly renews a series of tax cuts that were already legislated during the tycoon’s first administration, in 2017.

Donald Trump’s tax bill was approved by a narrow majority in the House of Representatives and is now ready to be analyzed by the Senate, where the Republicans have a majority. Specialists warn that in the event that the United States applies these increases to Chile, investors may not be protected by the agreement that prevents double taxation between the two countries.

Its length of more than 1,000 pages and the large number of topics it addresses has caused the analysis to focus on various measures, but there are some specific ones that could affect the interests of Chilean taxpayers who invest in the United States.

This is the new “Section 899”, a regulation that, among other aspects, imposes tax measures against investors from countries that adopt taxes defined as “unfair” towards U.S. companies and individuals.

The subject was addressed by the director of the tax area of PAGBAM | Schwencke, Maximiliano Concha, in a column in DF Tax last week, where he explained that among the taxes that may be increased are those levied on dividends, interest, royalties, business profits and real estate gains, which could even reach 50% as long as the tax considered “unfair” by the American tax administration is not eliminated.

What worries the most

From the Chilean point of view, the most “delicate” aspect of the proposed reform is the so-called revenge tax, explains Osiel González, a partner at Bruzzone & González Abogados.

“This tax seeks to tax with up to an additional 20% the income obtained by residents of countries considered discriminatory; that is, that impose unfair or discriminatory taxes on companies or individuals residing in the United States. The determination of the countries that will be affected will be the responsibility of the Department of State,” it explains.

Among the taxes that could be considered discriminatory, specialists point to the levy on digital services, existing in Chile and the global minimum tax that the OECD intends to implement.

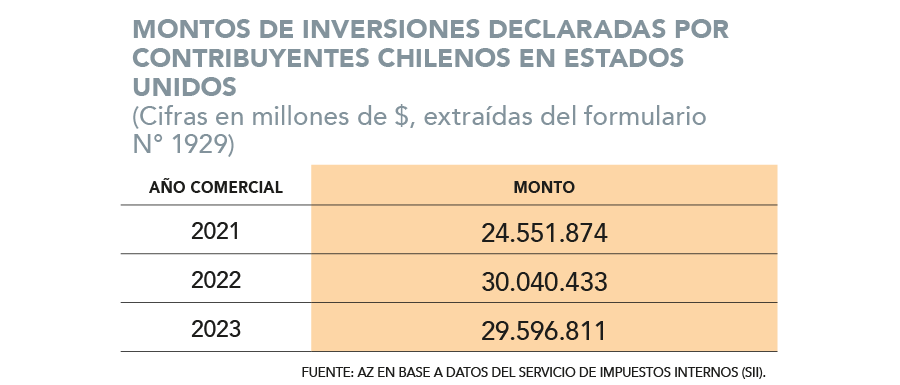

The director of the Tax Group of Albagli Zaliasnik (AZ), Andrea Bobadilla, explains that currently a distribution of profits from the United States to Chile is affected with a reduced rate of 5%, according to the agreement that avoids double taxation between both countries, which could be progressively increased up to 20%, which translates into more tax payments before bringing it to Chile, being able to use them as a credit.

“If before an investor received US$ 950 out of every US$ 1,000 for his investment, with this reform he could receive only US$ 800. In addition, it could affect other types of operations such as financing (loans), financial assets, operations taxed with digital services, among others”, the specialist explains.

For the International Tax partner of Deloitte Chile, Joseph Courand, it seems that Chile does not have taxes considered unfair, so Chilean investments would not be affected in principle, although the specific definition of digital taxes needs to be reviewed.

“A relevant aspect to consider is the possibility of Chile being categorized as a jurisdiction that imposes taxes considered unfair on U.S. citizens or residents. In that case, the U.S. tax authority could increase the withholding rate applicable to taxpayers resident or domiciled in Chile by up to five percentage points per year, with a cumulative maximum of 20 percentage points. This increase would affect payments made from the United States for interest, royalties, dividends and those related to real estate investments, among others”, he complements.

Mauricio Valenzuela, a partner in PwC Chile’s Legal and Tax Department, adds an additional factor of concern: that the increase would apply even to reduced withholding rates that are applicable under the aforementioned treaty that prevents double taxation between Chile and the United States.

“Likewise, the new rules propose to significantly extend the scope of application of the so-called BEAT (Base Erosion and Anti-Abuse Tax), which applies a tax to U.S. companies on tax deductions with foreign related parties (for example, a Chilean holding company), to the extent that certain requirements are met. This, by the way, would imply an increase in the tax burden in the United States”, he explains.

What clients are asking

Trump’s bill was approved by a narrow majority in the House of Representatives and is about to start its discussion in the Senate, where the Republicans are in the majority. As a result, clients of tax and legal firms have increased their inquiries regarding the initiative’s progress.

It is an issue that has Chileans who have direct financial investments or through investment companies in that country expectant, emphasizes the leading tax partner of Grant Thornton Chile, Francisca Pérez Navarro, but also those who have business operations in that country: “The reform could seriously affect the return on their investments, forcing them not only to leave the USA, but eventually to pay taxes prematurely if they have to liquidate their investments or close operations”, she warns.

EY Chile’s International Tax partner, Felipe Espina, points out that one concern is how the U.S. government will define the countries to which it will apply the new rates.

“For these purposes, a list of countries that are understood to apply unfair taxes to the United States would be published. It should be noted that the test for the application of the penalty would not only look at the country of the direct owner of the investment in the United States (or the recipient of payments subject to withholding tax), but would also look at the country of the indirect owner of the investment (with certain thresholds),” he adds.

It is thought that the double taxation treaty could protect investors from this reform, but the reality is that U.S. domestic laws may prevail over treaties according to their legal system, warns SW Chile partner Rodrigo Benítez: “It should be considered that the United States is the preferred destination for Chilean investors in financial instruments or real estate and the risk is real”.